Delayed Home Loan Disbursement 2026: How Builder Delays Impact Your EMI & Pre-EMI Interest

Is your home loan disbursement delayed by the builder? Discover how tranche delays impact your EMI, Pre-EMI interest, and real estate ROI in 2026.

The Fortune Realty Group

3/18/20264 min read

Delayed Home Loan Disbursement 2026: How Builder Delays Impact Your EMI & Pre-EMI Interest

Is your home loan disbursement delayed by the builder? Discover how tranche delays impact your EMI, Pre-EMI interest, and real estate ROI in 2026.

Table of Contents

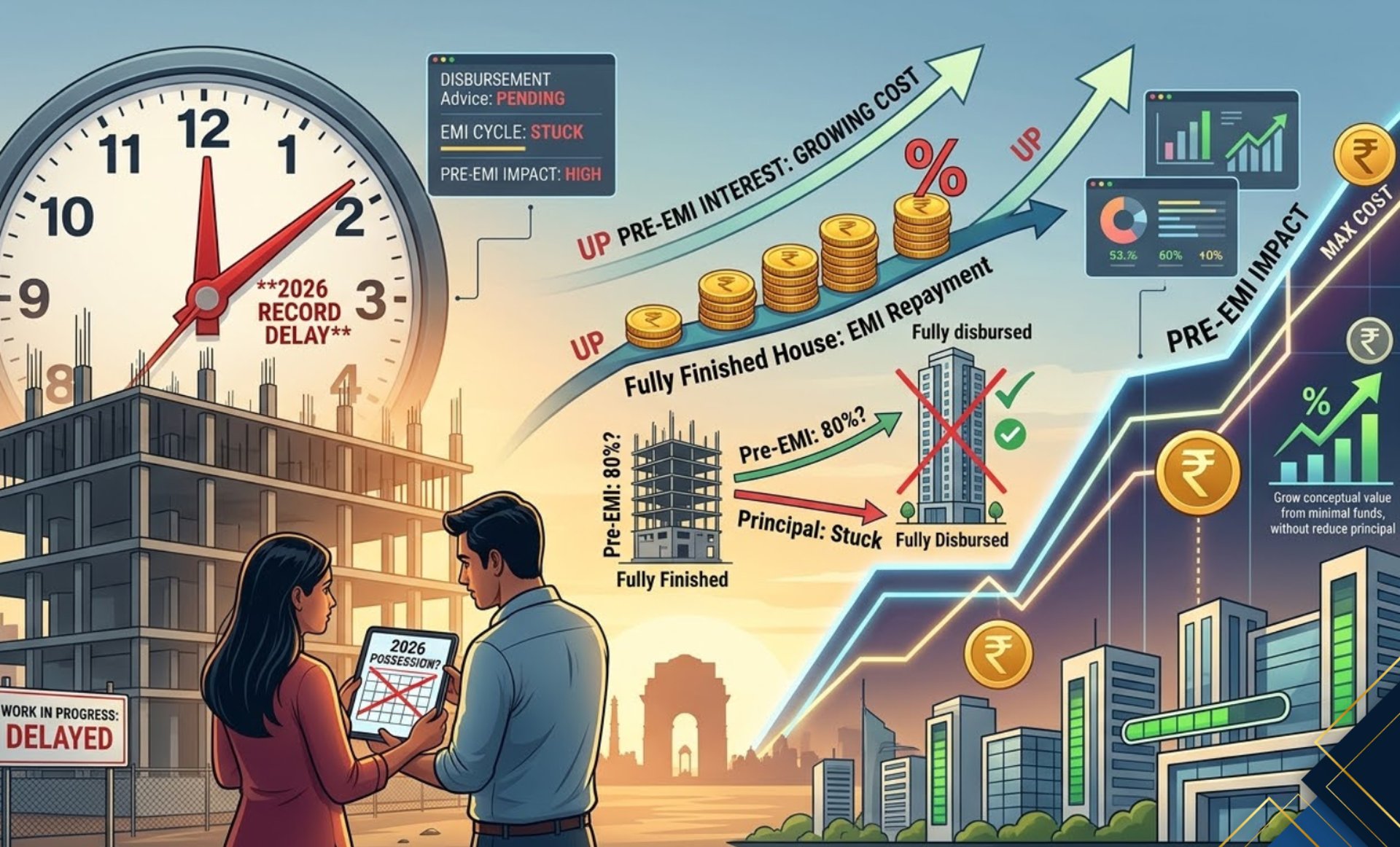

Receiving a home loan sanction letter is a major milestone, confirming that the bank is ready to fund your real estate investment. However, a frustrating gap often exists between this initial approval and the actual home loan disbursement to the builder. For buyers investing in under-construction properties, these administrative or builder-driven delays raise a critical financial question: Will the bank start charging my monthly instalments even if the money hasn't been released?

The short answer is no. The fundamental rule of borrowing is that you only pay for what you use. However, a home loan disbursement delay can still severely impact your repayment schedule, tax planning, and overall real estate ROI. Here is everything you need to know about how these delays affect your finances in 2026.

The Trigger: Why Disbursement Dictates Your EMI

An Equated Monthly Instalment (EMI) consists of two parts: the principal repayment and the interest. Legally, a bank cannot charge you for capital they have not transferred. Your loan agreement outlines a "repayment commencement date," which is directly triggered by the disbursement type:

Full Disbursement: Common for ready-to-move-in properties. The bank releases the entire amount at once, and your full EMI cycle starts the following month.

Partial Disbursement: Standard for under-construction projects. The bank releases funds in tranches (stages) based on specific construction milestones. If a builder fails to meet a milestone, the bank holds the funds, and your full EMI start date is pushed into the future.

If you are buying an under-construction property and have already received a partial payment, you enter the pre-EMI phase. During this period, you are only required to pay the interest on the small portion of the loan that has been disbursed.

While a delay in the final payment simply extends this pre-EMI phase, it is a hidden financial drain. Long pre-EMI phases are technically considered "dead money." Because you are only paying interest, your payments do not reduce your actual loan balance. They merely keep the loan active while you wait for the builder to finish construction, inflating your overall borrowing costs.

The Pre-EMI Trap: Beware of "Dead Money"

Even after signing the contract, the flow of funds can stall during the bank's final verification checks:

Technical Evaluations: The bank's engineer may visit the site and find that the actual construction progress does not match the builder's demand letter.

Missing NOCs: The builder might delay providing specific No Objection Certificates (NOCs) required by your lender.

Legal Discrepancies: The bank's legal team might uncover issues with the mother deed or updated property tax receipts.

Why Do Disbursement Delays Happen?

Beyond the pre-EMI interest drain, builder delays carry two major financial risks:

Loss of Tax Benefits: You can only claim tax deductions under Section 24(b) once you take physical possession of the property. If a disbursement and construction delay pushes your possession date into the next financial year, you completely lose a full year of valuable income tax benefits.

Sanction Letter Expiry: Most sanction letters are only valid for six months. If the delay drags on, your bank may require fresh income documents (salary slips, bank statements) to revalidate the loan. Worse, they could revise your interest rate if market conditions have changed, or charge a hidden "commitment fee" for not utilizing the funds within a specific window.

The Hidden Financial Impacts on Your Pocket

If your funds are stuck, stay proactive. Coordinate immediately between your builder's demand team and your loan officer. Ensure the builder submits demand letters the moment a floor is cast, and keep your financial documents updated to avoid sudden sanction letter expirations.

Actionable Steps for Homebuyers

To deepen your understanding of Delhi-NCR’s real estate trends and premium markets, explore these TFRG insights:

Home Loan Tax Benefits 2026: The Ultimate Guide to Claiming Stamp Duty & EMI Deductions

Haryana Property Tax Online 2026: Step-by-Step Payment Guide & Top Rebates via ULB Portal

Delhi-Meerut Expressway Real Estate Boom 2026: How Slashed Commutes Drive Massive ROI

Dwarka Real Estate Boom 2026: How 'Yashobhoomi' Skyrocketed Property Prices & ROI in 3 Years

India’s Most Expensive Retail Location 2026: The Massive ROI Behind Delhi’s Khan Market Real Estate

Top Premium Coworking Spaces in Noida 2026: The Ultimate Guide to Flexible Workspaces

Related Reads to Explore

Explore Other Prime Real Estate Opportunities in NCR

There are several verified and ready-to-move flats available in the region. At The Fortune Realty Group, we provide expert guidance and curated listings to help you find the perfect property.

You can explore:

Flats in Chattarpur & Vasant Kunj – Affordable options with excellent metro connectivity.

Farmland in Manesar – Ideal for investment and weekend retreats.

At The Fortune Realty Group, we help you find:

✅ Verified luxury builder floors with clear registry

✅ Prime locations like Gurugram, Manesar, Chattarpur, Vasant Kunj, Vasant Vihar, and more emerging hotspots

✅ Full support with home loans, legal formalities, and after-sales services

✅ Zero brokerage deals — so your investment goes directly into your dream home, not middlemen

With booming infrastructure, excellent connectivity, and rising demand, Gurugram, Manesar, Chattarpur, Vasant Kunj, and Vasant Vihar have become top choices in Delhi NCR for luxury living and high-return real estate investments.

Verified luxury builder floors with clear registry

How TFRG Makes Luxury Buying Stress-Free

Looking to Invest in South Delhi or Manesar?

Contact TFRG today for verified listings, legal due diligence, and best-in-class guidance across residential, commercial, and plotted developments.

The Fortune Realty Group

Experience hassle-free property deals with zero brokerage.

Contact Us

Inquiry

support@thefortunerealtygroup.com

+91-9990990317

© 2025. All rights reserved. Designed by PC Media House.